3 to back, 1 to skip — decided before a dollar moved.

Followers, fees, and a column of question marks.

Real reach × your store economics = profit — and the one loss it just caught.

The anomaly

Every channel earns a measurement layer. It becomes the giant.

In every channel, the company that owns the money question — what will this return, what should I pay, did it work — becomes the giant. Creator marketing has directories to find creators and CRMs to run campaigns. Nobody owns the money question. That empty seat is the company.

Search→Google Analytics

Email→Klaviyo · $9B

Paid social→Triple Whale

Creators · $33B→? still empty

Modash, GRIN & ShopMy exist — but they do search & workflow, not the money layer.

flows to creators every year — allocated almost entirely on guesswork.

2020$9.7B

2021$13.8B

2022$15B

2023$17B

2024$24B

+35% / yr

2025$33B

60%

of brands say ROI measurement is their #1 challenge

0

platforms can forecast a deal's profit before signing — Modash, GRIN, HypeAuditor included

$5K/mo

the typical agency retainer — and the decision still ends in that spreadsheet

Statista, Global Influencer Marketing Spend 2020–2025 · Sprout Social / eMarketer / IMH benchmark surveys.

The wedge

We answer the one question they can't get anywhere: will this creator make me money?

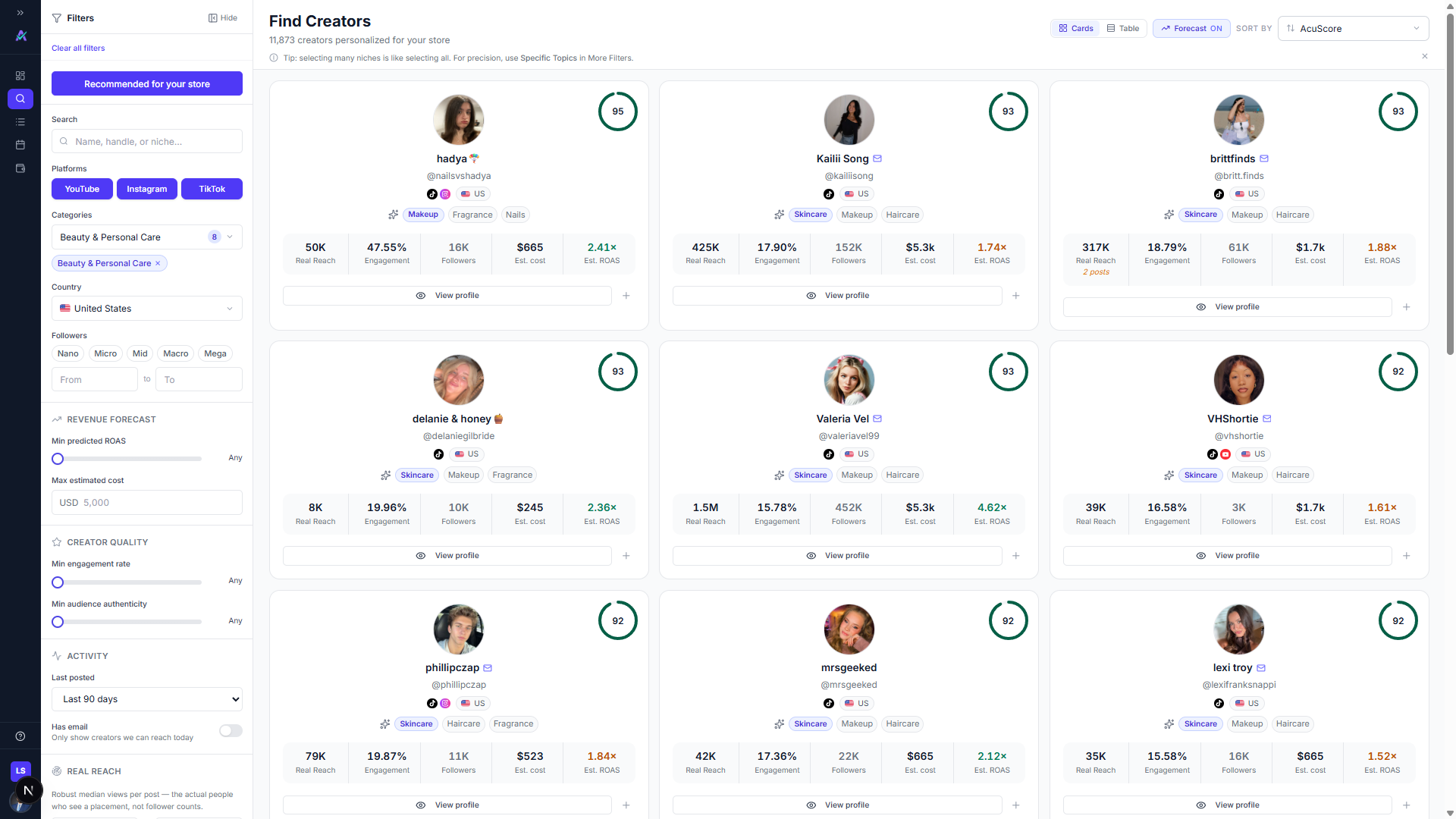

app.acurrate.com/discover

Every creator is ranked for this store by AcuScore — fit × quality × the revenue they'll drive — and every row carries its own profit forecast: real reach, estimated cost, estimated ROAS. Not follower vanity; the money math, on your store's real economics, across 140,000 creators we own outright.

Live product, June 2026 — real connected store (Luma Skin), real catalog.

How the forecast works — every number derives from the one above

From real views to a verdict. No black box.

It starts from the views that actually show up — robust median views, not follower counts — and walks to profit in four auditable steps, on your store's numbers.

46,400

median views (recent posts, robust)

→

418

clicks × 0.9% CTR

→

9

customers × your 2.1% conversion

→

$2,870

12-mo gross profit × your AOV, margin & returning rate

→

+$1,847

predicted profit after the $1,023 fee — before anything is signed

AOV, conversion and returning-customer rate pull from Shopify automatically — so the forecast runs on your real store economics, not category averages. It's the one number no competitor can put on screen.

One platform, the whole job

The decision is the wedge. The lifecycle is the lock-in.

Discover

140K creators, ranked

Forecast

profit before you sign

Negotiate

the fee that hits target

Agreement

AI draft + e-sign

Plan

schedule the year

Pay

money moves

app.acurrate.com/discover

Step 1 / 6 · Discover

Find the ones that'll make money.

140,000 creators we own outright, ranked by AcuScore — fit × quality × the revenue they'll drive on your store. Not follower vanity: the money math, on your economics.

Next: click Forecast →

Discovery + contracts + payments — $500–2,000/mo across three stacked tools elsewhere. Acurrate is all of it, one login, $99 flat.

Wedge → rail

The subscription is the foothold. The money flowing through is the business.

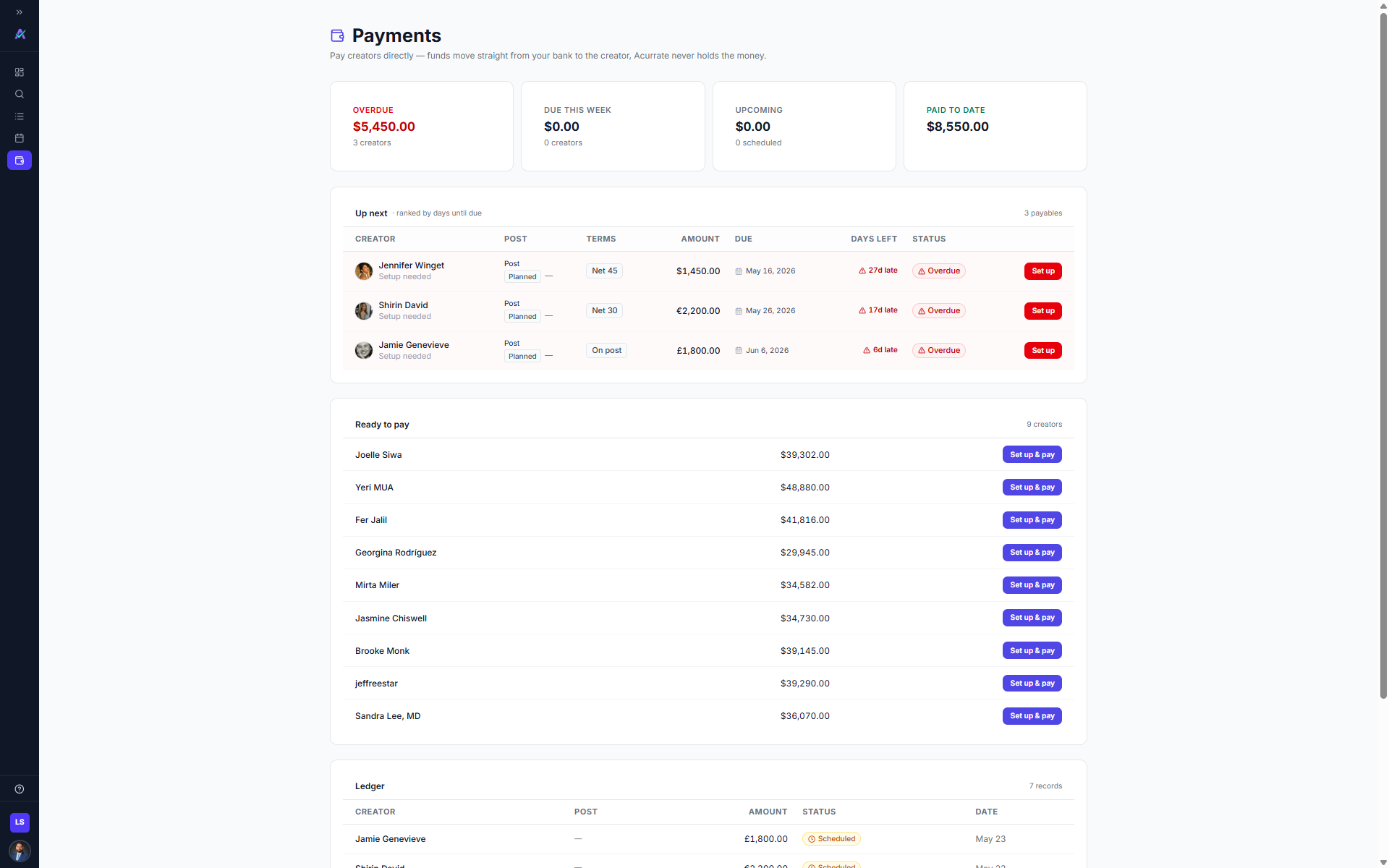

app.acurrate.com/payments

Once we sit at the decision, we own the payout. The Pay surface is built and live in-product — creator payments already run through it. The monetization switch — a ~0.75% net facilitation fee on every dollar — flips on in Year 2, once volume is proven. We never touch the float.

2–5×

revenue per customer once payments attaches

7–12×

ARR multiple for vertical SaaS + fintech (2026)

73%

of Shopify's revenue is merchant solutions, not subscriptions

The Toast / Shopify / ShopMy playbook: land with cheap software, expand into payments. We're already on it.

Three locks opened at once. You couldn't have built this 18 months ago.

Three things had to be true at the same time for this company to exist — and all three only became true in the last 18 months. That's the window we're raising into.

2020 → 2025

Spend hit critical mass

$9.7B → $33B. Creator marketing became a board-level budget line, not an experiment — so the ROI question became urgent.

May 2026

Shopify unlocked the data

Protected Customer Data L2 approval lets us pull a brand's real AOV, conversion and margin in one click. The data the forecast needs didn't flow before.

Now

AI collapsed the cost floor

Self-hosted scraping + distilled ML took the all-in cost of building a creator dataset to ~$0.003 a creator. A $99 flat price became viable where incumbents need $399+.

Shopify PCD L2 program · as-built data costs: ~$0.0029/creator blended ingest+enrich (self-hosted YT scrape via DataImpulse + TT/IG + distilled-ML/Gemini classify).

The structural tailwind

Privacy rules are dismantling tracked ads. Creator audiences don't need tracking.

A gardening channel is a perfectly-targeted audience of gardeners — forever. No cookie, no consent banner, no ad blocker, no new law can switch that off. The targeting is the content.

So the money is moving: 74% of brands are shifting budget into creator programs in 2026 — into the one channel that still has no measurement layer. Both tailwinds blow our way.

$10B / yr

what one privacy switch — Apple's ATT — cost Meta's ad engine in a single year

19 states

now have comprehensive privacy laws, every one with a targeted-ads opt-out — plus GDPR across Europe

1.7B people

run ad blockers. Creator content can't be blocked — it is the content

+40%

e-commerce customer-acquisition-cost inflation since 2023 as ad targeting degrades

They can't follow us to $99. Their payroll won't let them.

Monthly burn — drawn to scale

GRIN · 200+ ppl$2.5M+/mo

HypeAuditor · ~100 ppl$1.2M+/mo

Modash · ~50 ppl$500–700K/mo

Acurrate · 1 founder + AI team$230/mo

true bar = 0.1px — drawn bigger so you can see it

~$18K, once

builds the entire 5M-creator dataset — the same data an incumbent runs hundreds of staff to maintain. ~$0.003 a creator, all-in.

$0 / year

data licensing — we own the catalog outright (~$450/mo to run); incumbents rent theirs, forever

$99 flat

one price, 2 seats included (+$9/extra) — vs Modash/GRIN per-seat at $399–1,000+. 14-day free trial, no card.

~2 hrs

per feature, AI-supervised build — vs their 10–30 engineer-hours

Headcount/burn: public team pages + loaded-cost estimates. Acurrate $230/mo = today's actual cash cost (pre-raise, founder unsalaried); the post-raise operating plan is in The Numbers. Modash entry price doubled to $399, July 2026.

The market — bottom-up, not hand-waved

Shopify is the wedge. The market is every brand running creators.

$33B / yrcreator spend · +35%/yr

~$1.3BTAM · software + payments

$119MSAM · Shopify ICP today

$2.8MSOM · base case, Year 3

TAM → SAM → SOM. The base case captures a fiftieth of the beachhead alone.

Massive TAM, disciplined wedge

The forecast engine isn't Shopify-locked — it runs on any brand's economics. Shopify auto-fills them; everyone else connects another platform or types them in.

So the same product expands to every e-commerce platform, then every brand running creators — the market Modash and GRIN already proved is billions, where none of them can forecast profit.

We start on Shopify because we have the data + distribution edge there

Statista creator-spend $33B (+35%/yr) · TAM ≈ ~1M+ brands worldwide running creator budgets × $1,188/yr + ~$250M payments at 0.75% of $33B (third-party brand-count source to be cited) · SAM: Shopify ICP ≥$50K/mo (~100K stores) · SOM: model base case.

De-risked, not a deck promise

It's all already built — before the round.

140,000+

Owned creator dataset

enriched, ours, zero licensing cost

6 surfaces

Live platform

Discover→Forecast→Negotiate→Agreement→Plan→Pay

Pay rail

Stripe Connect payouts

built & live; fee layer switches on in Year 2

Shopify ✓

App Store + PCD L2

approved; one-click store economics

UK ®

Registered trademark

Acurrate Limited, a real entity

$50K in

Anchor secured

family office, round open

Built solo by a former DTC CFO directing an AI engineering team. Replacement cost alone is $600–900K. The downside is bounded; the upside is a $33B rail.

The 5-year picture — the Shopify plan, then beyond it

Profitable in Year 2. Then it scales past Shopify.

$0.16M

Year 1Aug 26

$0.95M

Year 2breakeven

$2.1M

Year 3Shopify

$4.8M

Year 4+ expansion

$12M

Year 5illustrative

SubscriptionPaymentsEBITDA▦ Years 4–5 illustrative (beyond Shopify)

$2.8M

revenue run-rate, month 36

Sep-27

EBITDA-positive

95%

gross margin

2.4mo

CAC payback

9.9×

LTV : CAC

2,068

customers, month 36

$264K

cash trough — never near zero, in any scenario

24+ mo

survival runway at $0 revenue

Customers are an output of channel math — no hardcoded hockey stick. The full live model is in the data room; edit any assumption, it recalculates.

Acurrate model, June 2026 — Excel-verified, balance-sheet tied. Y1–3 = the bottoms-up Shopify plan (the raise stands on these). Y4–5 illustrative: other e-com platforms + global brands + the payments rail inflecting to ~26% of revenue.

Your return — stress-test it yourself

What a cheque today becomes. Bear to bull.

Your investment

$

6.1×

illustrative return at a Year-5 exit (~2031) · $25,000 → $152K

Entry on a SAFE at the $5M post-money cap (20% discount = extra upside). Your stake rides every round; ownership dilutes, value compounds.

How this is calculated →

Illustrative scenarios, not a forecast or an offer of securities. Round valuations = the model's projected ARR (Year-4/5 illustrative) × labelled 2026 vertical-SaaS+fintech multiples, less stated dilution. Even the Bear case clears the entry cap at every round.

The ask

$500K · $5M post cap · 20% discount.

$50,000 secured · 10% — family-office anchor

$300K = fully operational · $500K = full speed

Instrument: YC SAFE (US) / ASA (UK, SEIS-eligible) · MFN · ~10% dilution at cap. Why the cap is fair: rebuilding the asset alone costs $600–900K — the cap is ~6× that, with the dataset, Shopify approvals and live rail included. Runway: 24+ months → profitable → next round from a position of power, not need.

$500K

use of funds

Founder salary · 40%

Sales & GTM (AE, growth, ads) · 37%

Customer success · 11%

Infra + data (the cheap moat) · 6%

Legal + reserves · 6%

Let's build the platform every brand runs creators on.